Definitive Glossary of Project Financial Management Terms

Projects do not go off budget in one dramatic moment. The damage usually starts earlier, in small language failures that teams overlook: cost baseline confused with budget, reserve mixed up with funding, forecast treated like actuals, earned value reported without context, and change impact discussed without a financial control frame. Once those terms get blurred, approvals slow down, reporting turns cosmetic, and leadership loses trust in the numbers.

This glossary fixes that problem. It breaks down the financial management terms project managers need to control budgets, forecast pressure early, defend decisions, and speak with real authority when money, scope, timing, and stakeholder expectations start colliding.

1. Why Project Financial Language Decides Whether a PM Looks Credible or Lost

A project manager can survive weak charisma longer than weak financial control. Teams forgive a quiet PM. Sponsors do not forgive one who cannot explain where the money went, what the current burn means, whether reserves are being consumed too early, or how a scope change affects total exposure. That is why project financial management terminology matters far beyond exam prep. It governs decision quality.

Too many projects operate with a fake sense of budget awareness. The team knows the approved number, tracks invoices, and holds a monthly cost meeting, so everyone assumes the project is financially controlled. Then vendor costs land earlier than planned, internal labor is undercounted, procurement timing distorts the burn pattern, contingency gets spent on preventable slippage, and the reporting pack still says the project is “within budget.” That is not control. That is delay between damage and recognition.

A financially strong PM understands how cost terms connect to essential project budgeting terms, top 20 cost management terms for project managers, comprehensive project risk management glossary, and critical project stakeholder terms every PM should master. They also know financial control is inseparable from project scheduling terms, critical path method terms, project procurement terms & definitions, and contract management terminology, because money rarely fails alone. It fails through time, decisions, and dependencies.

This article gives you the terms that matter when a sponsor asks whether the project is still financially viable, whether a change request is affordable, whether contingency use is justified, and whether the current forecast can still be trusted.

| Term | Meaning in Practice | Why It Matters | Typical PM Use |

|---|---|---|---|

| Budget | Approved spending limit for the project | Defines financial boundaries | Baseline for control and reporting |

| Cost baseline | Time-phased approved budget used for measurement | Supports variance tracking | Compared against actuals and earned value |

| Funding | Money made available to support project work | Impacts timing and cash flow | Used in release and stage planning |

| Cash flow | Timing of money moving in and out | Prevents liquidity surprises | Vendor payment and milestone planning |

| CapEx | Capital expenditure tied to long-term assets | Changes approval and accounting treatment | Large systems or infrastructure buys |

| OpEx | Operational expenditure for ongoing costs | Affects sustainability and ownership | Licenses, support, subscriptions |

| Direct cost | Cost tied directly to project work | Improves cost traceability | Labor, materials, contractors |

| Indirect cost | Shared or overhead cost not tied to one task | Prevents underestimating total cost | Facilities, admin support |

| Fixed cost | Cost that does not vary with output in the short term | Improves planning stability | Contract fee, setup charge |

| Variable cost | Cost that changes with volume or effort | Improves forecast realism | Usage-based services, overtime |

| Cost estimate | Predicted financial requirement for work | Drives approvals and planning | Bottom-up or analogous estimating |

| Estimate at Completion (EAC) | Forecasted total project cost at finish | Signals final exposure | Used in sponsor reporting |

| Estimate to Complete (ETC) | Expected remaining cost from today forward | Improves recovery analysis | Used in reforecasting |

| Actual Cost (AC) | Money actually spent to date | Grounds reporting in reality | Compared against baseline and EV |

| Planned Value (PV) | Budgeted value of scheduled work | Shows financial plan at a point in time | Used in earned value analysis |

| Earned Value (EV) | Budgeted value of work actually completed | Connects cost and progress | Measures execution performance |

| Cost Variance (CV) | Difference between EV and AC | Shows overrun or underrun | Tracked in status reports |

| Schedule Variance (SV) | Difference between EV and PV | Shows progress slippage | Used with cost analysis |

| Cost Performance Index (CPI) | Efficiency ratio of EV to AC | Shows spending efficiency | Used in forecasting formulas |

| Schedule Performance Index (SPI) | Efficiency ratio of EV to PV | Shows pace of delivery | Used with schedule recovery planning |

| Contingency reserve | Time or money for known risks | Protects against expected uncertainty | Released when risk materializes |

| Management reserve | Extra budget for unknown unknowns | Provides executive financial buffer | Controlled outside normal baseline |

| Burn rate | Speed at which budget is being spent | Reveals pressure early | Used in monthly finance reviews |

| Committed cost | Amount legally or operationally obligated | Prevents false budget optimism | POs, signed contracts, approved change orders |

| Accrual | Recognized cost before invoice payment timing | Improves true cost visibility | Month-end financial close |

| Variance analysis | Investigation of gaps between plan and reality | Prevents repeated surprises | Root cause review and action setting |

| Cost control | Process of influencing and managing spend | Protects project viability | Approvals, monitoring, corrective action |

| Change order | Formal change affecting price, scope, or time | Protects financial integrity | Used in vendor and contract shifts |

| Cost-benefit analysis | Comparison of expected cost against value | Improves decision quality | Business case and change review |

2. Core Budget and Cost Terms Every PM Must Understand Cold

A budget is the approved financial limit for the project. Straightforward on paper, messy in practice. Teams keep saying “we have budget” when they really mean funds exist somewhere in the portfolio. That is not the same thing as approved project-level budget authority. A PM who confuses funding availability with authorized project budget will make commitments too early and end up apologizing later.

A cost baseline is even more important. It is the approved, time-phased budget used for measuring performance. This is what lets a PM say whether current spend is happening at the right pace, not just within the overall cap. A project may still be inside the total budget and still be financially unhealthy if spend is landing far too early. That is why baseline control has to connect with project scheduling terms, critical path method terms, project reporting & analytics software, and dashboard & data visualization tools.

A cost estimate is the predicted financial requirement for work. Good PMs treat estimates as structured judgments shaped by scope maturity, risk, vendor knowledge, labor assumptions, and schedule realism. Weak PMs treat them like promises. That is how projects get approved on polished optimism and then bleed credibility later. Estimating gets stronger when the PM also understands top 25 risk identification & assessment terms, project failure rates & root causes, project success drivers, and top challenges facing project managers today.

Then come direct costs and indirect costs. Direct costs are attributable to project work itself, such as assigned labor, contractor fees, or materials. Indirect costs cover shared services and overhead. Teams underestimate project financial reality when they track only what is obviously visible in the workstream and ignore support functions, governance overhead, environment costs, and compliance effort. That gap becomes brutal on complex or regulated programs.

You also need to distinguish fixed costs from variable costs. Fixed costs do not move much in the short term. Variable costs rise or fall with usage, workload, or output. This distinction matters during scope shifts and recovery plans. A PM who knows what part of the cost structure is elastic can negotiate smarter.

3. Forecasting and Earned Value Terms That Reveal Trouble Earlier Than Gut Feel

Most projects do not need more status meetings. They need cleaner forecasting. This starts with Actual Cost (AC), the money actually spent so far. That sounds obvious, but many teams report actuals with incomplete invoice capture, lagging accrual logic, or missing internal labor. When actual cost data is weak, every downstream forecast gets polluted.

Planned Value (PV) tells you the budgeted value of work that should have been completed by a point in time. Earned Value (EV) tells you the budgeted value of work actually completed. That distinction is where superficial reporting gets exposed. A team can claim progress loudly while earning very little value relative to plan. That is why earned value matters. It links financial control to real delivery, not presentation quality.

Cost Variance (CV) measures the gap between earned value and actual cost. Schedule Variance (SV) measures the gap between earned value and planned value. Cost Performance Index (CPI) and Schedule Performance Index (SPI) turn those gaps into efficiency ratios. These are not vanity metrics. They help answer the questions leaders actually care about: Are we spending efficiently? Are we progressing at the right pace? Is the project becoming harder to recover with every reporting cycle?

Projects that use project issue tracking software, project budget tracking software tools, project management software for healthcare projects, and PM software for the software development industry often have more data available than they realize. The problem is not missing systems. The problem is failing to translate those numbers into useful financial narratives.

That leads to Estimate at Completion (EAC) and Estimate to Complete (ETC). EAC forecasts the expected total project cost at the end. ETC forecasts what it will take from today onward. These matter most when a project is no longer following its original assumptions. A PM who keeps repeating the original budget after productivity dropped, vendor pricing moved, or change requests stacked up is not demonstrating discipline. They are broadcasting denial.

Budget pressure rarely begins with one giant mistake. It builds through small financial blind spots that nobody forces into the open early enough.

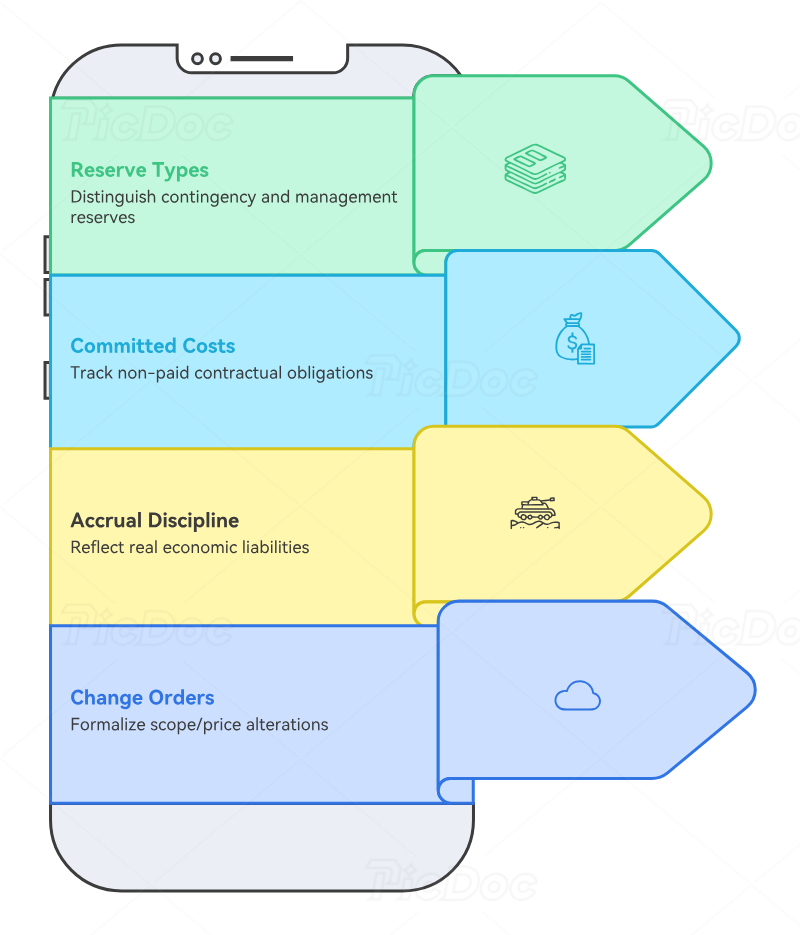

4. Reserve, Commitment, and Change Terms That Protect the Budget From False Confidence

A financially mature PM treats reserves with precision. Contingency reserve is money or time set aside for known risks. Management reserve is held for unknown uncertainty outside the baseline. Teams weaken trust when they use these terms interchangeably. If vendor instability, approval delays, or design rework are already visible risks, the response funding belongs in contingency logic, not hidden under vague “buffer” language. That thinking should connect directly to risk management glossary, risk identification terms, project procurement terms, and contract lifecycle management software.

A committed cost is an obligation already created even if cash has not left yet. Signed statements of work, purchase orders, approved change orders, and fixed delivery commitments all matter here. Projects often look financially healthier than they really are because the team reports only paid invoices and ignores committed exposure. That is how PMs get ambushed by “sudden” overruns that were contractually inevitable weeks earlier.

Accrual matters for similar reasons. A cost can be economically real before billing timing catches up. If work has been done and liability exists, a strong project financial picture should reflect that. Without accrual discipline, a project can appear clean at month-end and then take a financial hit later that should never have been a surprise.

Then comes the term that wrecks budgets faster than almost any other: change order. A change order is the formal mechanism that alters scope, price, time, or contract conditions. PMs who tolerate informal change discussion are practically inviting financial distortion. When stakeholders want “just one more enhancement,” when legal language changes after approval, when integration expands beyond the original statement, and when timeline compression requires premium staffing, those are not harmless tweaks. They are financial events. Teams need the discipline described in essential project communication terms & techniques, critical project stakeholder terms, best document management software, and best procurement management tools to keep those shifts visible and enforceable.

5. Decision Terms That Help PMs Defend Financial Choices With Authority

A PM should never sound trapped between accounting language and delivery language. The bridge term here is variance analysis. This is not just the act of noticing a gap. It is the discipline of explaining why the gap happened, whether it is structural or temporary, what it means for future performance, and what corrective action follows. When variance analysis is weak, the same mistakes repeat in every reporting cycle with different labels.

Burn rate tells you how fast the budget is being consumed. This matters most when a project is entering a rough phase, using expensive specialist labor, or front-loading procurement. A high burn rate is not automatically bad. A high burn rate without earned progress, however, is where finance and delivery both start losing patience.

A cost-benefit analysis compares expected cost against expected value. This is one of the most useful terms during changes, recovery options, tooling decisions, and staffing debates. The cheapest decision is often the most expensive one later if it increases failure risk, rework, or adoption resistance. Smart PMs weigh this with context from best automation tools for project management efficiency, top productivity software for busy project managers, future of project management software, and AI & automation adoption in project management.

Finally, there is cost control itself. Cost control is not bookkeeping. It is the process of influencing outcomes through approvals, monitoring, forecasting, corrective action, scope discipline, contract clarity, and leadership escalation. It depends on strong reporting, yes, but also on the courage to tell stakeholders when the numbers no longer support the story they want to hear.

6. FAQs About Project Financial Management Terms

-

A budget is the approved spending limit. A cost baseline is the approved budget distributed over time so the PM can measure performance period by period. One sets the ceiling. The other makes control possible.

-

Because actuals alone are not enough. Projects also need committed cost visibility, accrual accuracy, forecast discipline, reserve control, and change management. Tracking money already spent does not protect against money already obligated or future exposure already visible.

-

EAC shows where the project is likely to land financially, not where it started. It gives leadership a realistic end-state view. When a PM refuses to reforecast, the project becomes politically comfortable and financially dangerous.

-

It should be used when a known risk materializes or when preapproved response logic requires it. It should not become a casual pool for weak planning, soft scope creep, or avoidable execution errors that were never treated seriously.

-

CPI shows spending efficiency. SPI shows progress efficiency. Together, they expose a brutal truth quickly: whether the project is buying enough progress for the money and time already consumed.

-

Actual cost is what has been spent or recognized to date. Committed cost reflects obligations already created, such as signed contracts or purchase orders. A project can look safe on actuals while being heavily exposed on commitments.